Install our App to get easy Access toBuy, Link, Renew, Claim and More

Get

SRS Airbag: What It Is and Why It Matters for Your Car Insurance

May 21, 2026

Road accidents are often unpredictable and may lead to fatal injuries. Though collisions cannot always be avoided, their impact can be reduced by an efficient safety system. Seatbelts act as the primary restraint system in a car and are therefore essential. An SRS airbag acts as a supplemental restraint system offering further protection.

This article focuses on what SRS airbags are, how they work, their types and their connection with car insurance coverage and claims.

What is an SRS Airbag?

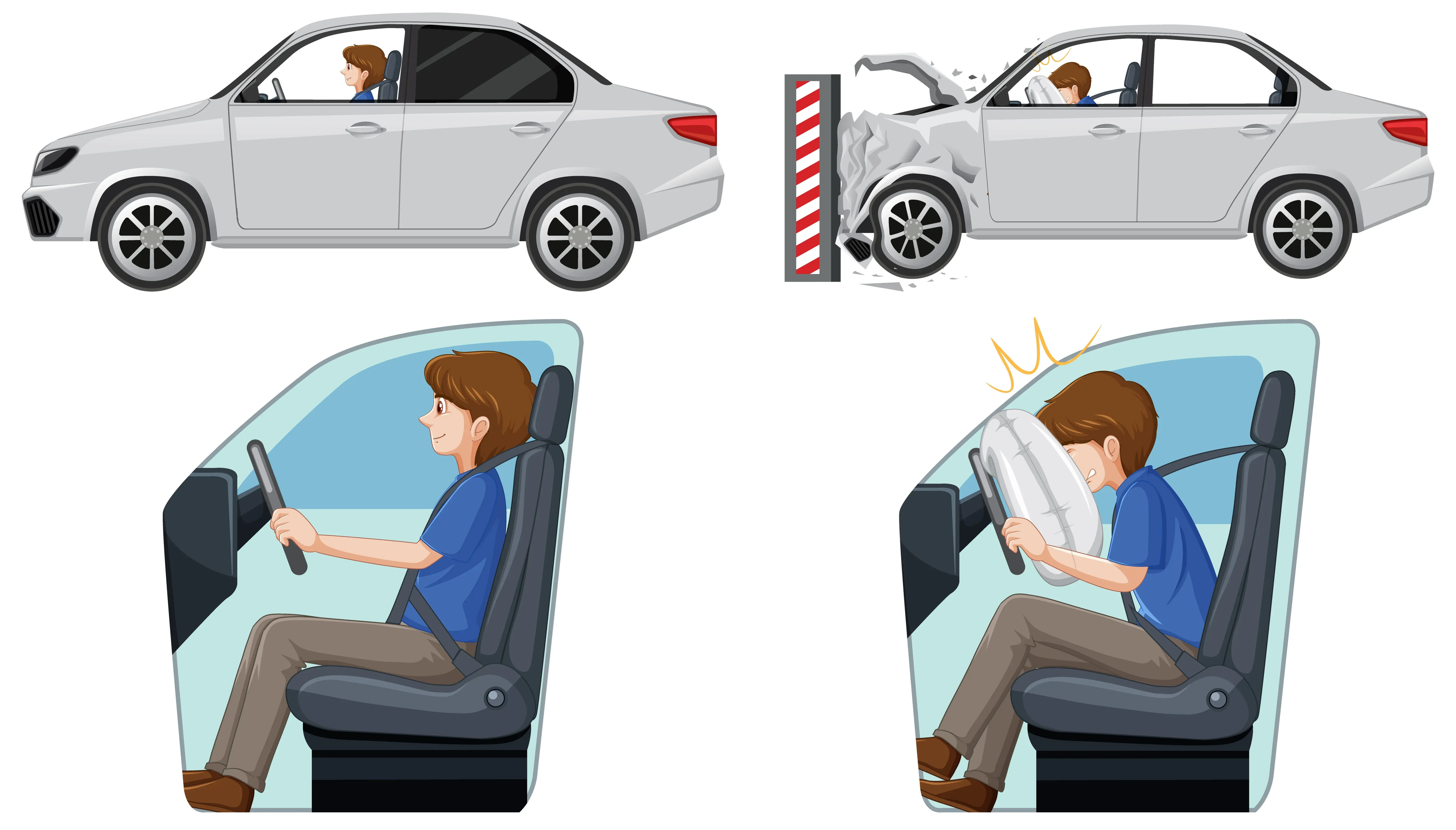

A Supplemental Restraint System airbag, or an SRS airbag, is a vehicle safety feature designed to provide additional protection to passengers during a collision. It can help reduce injury risks in accidents, particularly collisions. It works along with features like seatbelts, providing an extra layer of protection to drivers and passengers. These airbags can also influence vehicle repair costs and insurance claims after an accident.

Car manufacturers design an SRS airbag to inflate during collisions, shielding the occupant from injuries. It is located at the centre of the steering wheel, on the passenger side of the dashboard and in a few other locations.

The airbag is known as a ‘supplemental system’ because it is designed to work alongside the seatbelt rather than as a replacement.

How Does an SRS Airbag Work?

Now that the query ‘what is SRS airbag’ has been addressed, let us understand how it works. Typically, an SRS airbag relies on a sensor system to know when and how to deploy. These sensors are located throughout the car. They detect the following:

- Braking

- Impact location

- Deceleration

- The presence of a passenger

All information gathered by the sensor is processed by an algorithm that determines whether airbag deployment is necessary, and if so, how much force is required. When a collision is detected, the sensors send signals to the electronic control unit. This causes the airbag to inflate within a fraction of a second. After the collision passes, the airbags deflate.

Types of SRS Airbags in Cars

Rather than a single SRS airbag, modern cars usually come equipped with multiple airbags placed at different locations inside the vehicle to provide broader protection during a collision. These are some common types:

Front Airbags

These may include the driver's airbags, which are located in the steering wheel. They help protect the driver’s chest and head. Passenger airbags, located in the dashboard, offer protection to the passenger.

Side and Curtain Airbags

Side airbags protect passengers in side-impact collisions, while curtain airbags inflate and drop from the ceiling. This helps protect the head during a collision.

Knee Airbags

During an accident, the lower body is also at risk of injury. The knee bolster airbags have been designed to prevent this. They protect the front seat passenger and the driver.

Your car has advanced safety protection that may save you during accidents, but a third-party insurance can offer financial protection in case of liabilities that arise from injury, death or property damage to third parties.

SRS Airbag and Car Safety Ratings

The Global New Cars Assessment Program (NCAP) evaluates new vehicles across safety parameters. These often include safety belts, grown-up and kid occupant protection, electronic stability control, pedestrian protection, and so on. It offers a rating out of five to provide clarity about which vehicles are safe.

The effectiveness of the SRS airbag may be considered during such safety evaluations. Their effectiveness may be tested alongside seatbelt efficiency.

SRS Airbag and Car Insurance Premium

The importance of SRS airbag in car insurance is evident as it may influence motor insurance assessments. While calculating motor insurance premiums, insurers often evaluate the overall safety features of a vehicle. Cars equipped with safety systems such as SRS airbags, anti-lock braking systems (ABS), and stability control may be considered safer in certain situations. This may sometimes influence premium calculations depending on the insurer’s risk assessment policies.

However, having an SRS airbag alone does not automatically guarantee lower insurance premiums. Some insurers may not consider these features while calculating premium rates. Therefore, it is important to read the policy terms and coverage conditions carefully before purchasing car insurance.

Is Airbag Replacement Covered Under Car Insurance?

Car insurance may often cover the cost of airbag replacement. However, they are marked under specific categories, which at times creates coverage complications. For instance, when an accident is caused by the policyholder, the company, under collision coverage, provides assistance with the replacement or repair of the SRS airbag. However, if the opponent driver is at fault, their liability insurance coverage may cover the accidental expenses. It is best to read through the policy wording or reach out to your insurer for details.

SRS Airbag Warning Light: What to Do

When the SRS airbag warning light comes on, it may indicate a fault and that the airbags may not deploy in time. Common causes may include:

- Faulty sensors

- Damaged control unit

- Loose wiring

- Poor repairs after an accident

It is best not to avoid the light when it comes on and to limit driving till the issue is fixed. Consult an authorised technician and do not simply reset the light.

Conclusion

An SRS airbag is important to maintain driver and passenger safety. It functions efficiently along with seatbelts and may help reduce the severity of injuries during accidents. However, even with the presence of this feature, it is best to have an insurance policy. It can cover the cost of potential damage from an accident.

Vehicle owners can explore car insurance solutions from SBI General Insurance for financial protection against unexpected road-related risks.

Frequently Asked Questions

1. What does SRS stand for in airbag?

SRS stands for Supplemental Restraint System airbag. It refers to the vehicle’s entire airbag system, including the sensors and the control unit.

2. Does car insurance cover airbag replacement?

Comprehensive car insurance policies may cover airbag replacement costs if the airbags deploy during a covered accident, subject to the policy terms, conditions, and exclusions.

3. Does having airbags lower my car insurance premium?

Having airbags can lower car insurance premiums as they can reduce the severity of injuries. However, this reduction depends on the insurance policy.

4. What should I do if my SRS airbag warning light is on?

As this light indicates a fault has been detected, have the vehicle inspected promptly.

5. How many airbags does a safe car need?

Many modern safety standards recommend multiple airbags, as they offer comprehensive protection in both frontal and side collisions.

This blog is intended solely for educational and informational purposes. Content reflects data at time of publication and may not accurately reflect current premiums, terms, or regulations. Readers are encouraged to confirm the accuracy and relevance of the data before making any significant decisions. SBI General Insurance disclaims responsibility for any errors or consequences arising from the use of outdated information provided herein. For more details, please refer to the policy wordings and prospectus before concluding the sales. *Add-ons are subject to payment of additional premium.

Access and manage all your Insurance Needs in one place, right at your Fingertips.

4/5*

Access and manage all your Insurance Needs in one place, right at your Fingertips.

Vision

Our vision is to become the most trusted general insurer for a transforming India.

Mission

Our mission is to provide simple and innovative general insurance solutions, be responsive to our customers' needs and build a sustainable business for the future.

We're socially active!