Install our App to get easy Access toBuy, Link, Renew, Claim and More

Get

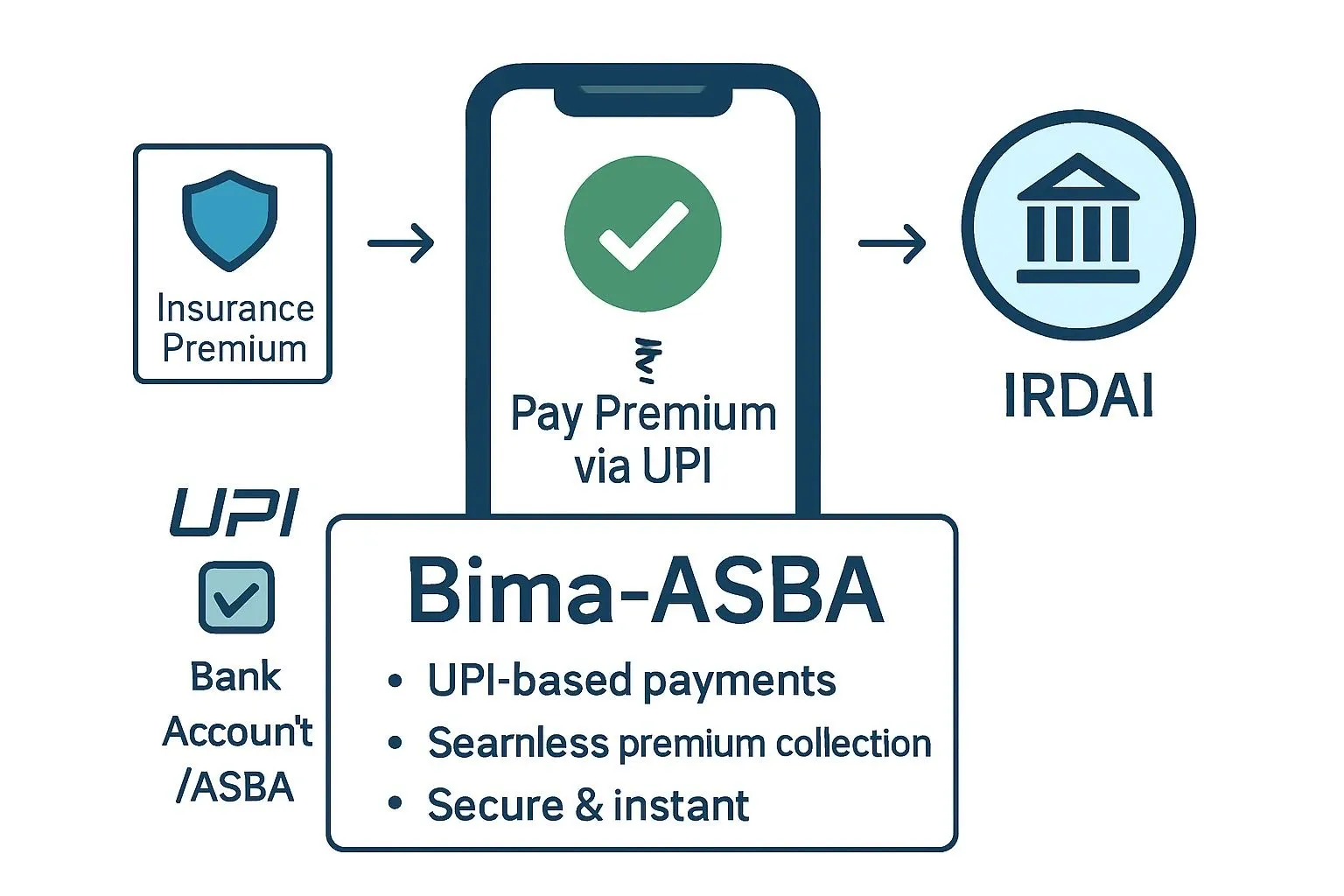

Bima-ASBA Facility: A New Standard for Insurance Premium Payments in India

Date: Jan 28, 2026 - Last Modified Jan 28, 2026

The Insurance Regulatory and Development Authority of India (IRDAI) has introduced a new mechanism for collecting insurance premiums called Bima-ASBA (Applications Supported by Blocked Amount). This system changes how insurers collect money during the policy issuance process.

From March 1, 2025, insurance companies are mandated to provide an option to the customers to block the premium amount in their bank account instead of paying it upfront. The amount is deducted only after the insurer completes underwriting and accepts the proposal. This process is enabled through UPI One-Time Mandates (OTM).

The change applies to Life and Health Insurance policies and is a part of IRDAI’s broader effort to improve transparency, reduce refund issues, and protect policyholder interests. At present the facility of BIMA ASBA is extended to individual policyholders.

Background and Regulatory Intent

According to the Circular:

- Insurers should collect premium only post acceptance of proposal.

- Risk shall commence from the date of acceptance of proposal.

- The circular also requires insurers to obtain express consent from customers before blocking the funds towards applicable premium payable and deducting any amount from their bank accounts upon acceptance of proposal.

How the Bima-ASBA Mechanism Works

Fund Blocking Instead of Immediate Debit

Under the Bima-ASBA system, the premium amount is not transferred to the insurer when the customer submits the proposal form. Instead, the amount is temporarily blocked in the customer’s bank account through a UPI One-Time Mandate.

The money stays in the prospect’s bank account, but it cannot be used for other transactions. This means the customer retains ownership of the funds while ensuring that a sufficient balance is available once the proposal is accepted.

Only after the insurer makes an underwriting decision and accepts the proposal, does the bank debit the blocked amount and transfer it to the insurer.

What Happens if the Proposal is rejected

If proposal is rejected, the amount is unblocked within 1 working day from the date of non-acceptance of proposal or auto unblocked after 14 days from date of blocking of funds.

In case proposal is cancelled by the prospect before underwriting decision, insurer shall release the unblocked amount within one day from day of request.

The money becomes fully available in the customer’s bank account again.

This automatic release of blocked funds reduces delays, prevents disputes, and ensures that customers are not financially impacted.

What is a UPI One-Time Mandate?

A UPI One-Time Mandate is a digital authorisation that allows a bank to block a specific amount in a customer’s account for a single, defined purpose. In the case of Bima-ASBA, this purpose is to block the insurance premium amount payable during the underwriting process.

The mandate ensures that the premium is not deducted immediately. This feature allows users to block funds in their bank accounts, ensuring availability of funds while deferring actual payment.

This system is designed to be secure and consent-based, meaning the customer must approve the mandate before any amount is blocked.

Key Features of UPI One Time Mandate

- Requires customer approval

- Funds stay in the customer’s account

- Debit occurs only upon acceptance of the proposal. Prospect is kept informed at every stage of BIMA ASBA i.e, blocking of funds, initiation of debit, unblocking of funds.

- This mechanism works in a similar way to the ASBA system used for IPO applications, where money is blocked but not transferred until final allotment.

Impact on Policyholders

Financial Control

Customers keep control of their money until the proposal is approved. There is no risk of paying for a policy till proposal is accepted.

No Refund Dependency

Since money is not debited upfront, there is no need for refund if the proposal is rejected or cancelled.

Mandate Expiry

If the insurer does not process the proposal within a period of 14 days, the blocked amount will be automatically unblocked through the partner bank by the insurer.

Additional Charges

No additional charges are levied for using the Bima-ASBA facility.

Summary of Key Regulatory Requirements

| Area | Requirement |

| Premium Collection | Only after underwriting approval |

| Risk Coverage | Begins from the date of acceptance of proposal |

| Customer Consent | Mandatory |

| Mandate Expiry | 14 days (if the insurer does not process the proposal) |

| Additional Charges | Not allowed |

| Policyholder Choice | Optional |

| Policy Types | Life & Health Insurance |

Conclusion

The Bima-ASBA framework represents a major improvement in how insurance premiums are handled in India. By shifting from upfront payments to a fund-blocking model, IRDAI has strengthened transparency, reduced refund complications, and ensured that customers only pay for approved policies.

Frequently Asked Questions

How does Bima-ASBA work?

Here’s the step-by-step process:

1. Choose the option to pay via Bima-ASBA when you apply for a policy.

2. Your insurer sends a request to your partner bank to block the premium amount via UPI’s One-Time Mandate (OTM).

3. You approve the block request in your UPI app.

4. The amount stays blocked but in your account until underwriting is done.

5. Once the proposal is accepted, the insurer debits the amount.

6. If the policy is rejected or not processed in time (max ~14 days), the amount is unblocked automatically.

What types of insurance can use Bima-ASBA?

Currently, Bima-ASBA applies to life and health insurance policies. The focus is on smoother, safer premium payments for these products.

Do I pay any charges for using it?

There are no extra charges specifically for using Bima-ASBA — it’s meant to make premium payments easier and more transparent.

What happens if the insurer delays or doesn’t make a decision?

If the insurer doesn’t complete underwriting within 14 days, the blocked funds are automatically released back to your bank account so your money isn’t held indefinitely.

What are the main benefits?

- No immediate debit from your account

- Your money remains in your account

- Automatic refund/unblock if the policy isn’t approved

- More transparency and less hassle compared to upfront payments and later refunds

How is BIMA ASBA different from other ways of payment?

With the introduction of BIMA ASBA, the premium amount is not transferred to the insurer when the customer submits the proposal form. Instead, the amount is temporarily blocked in the customer’s bank account through a UPI One-Time Mandate and is only debited on successful acceptance of the proposal.

Access and manage all your Insurance Needs in one place, right at your Fingertips.

4/5*

Access and manage all your Insurance Needs in one place, right at your Fingertips.

Vision

Our vision is to become the most trusted general insurer for a transforming India.

Mission

Our mission is to provide simple and innovative general insurance solutions, be responsive to our customers' needs and build a sustainable business for the future.

We're socially active!